Uranium Price Update: Q2 2025 in Review

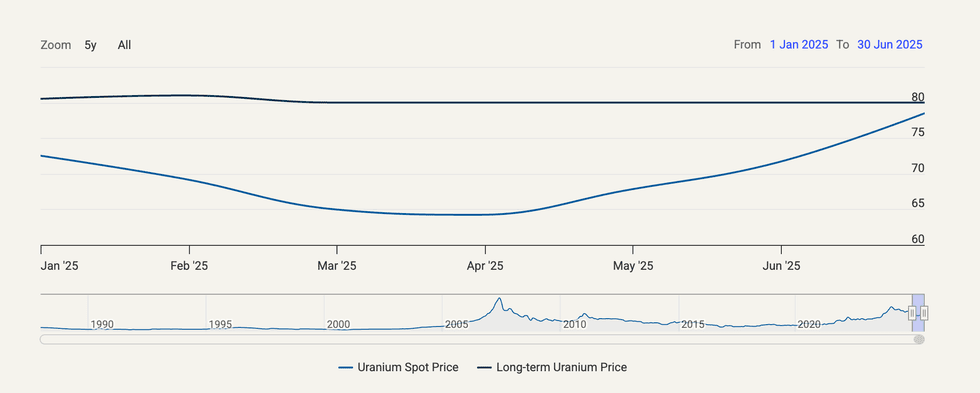

The uranium market entered Q2 on shaky footing, with spot prices slipping to around US$63.50 per pound (March 13)—the lowest level in 18 months—as utilities hesitated to contract amid ample secondary supply and demand uncertainty.

By early June, however, spot prices rebounded to the US$70–US$71 per pound range, buoyed by geopolitical tailwinds and renewed nuclear policy support in the US.

While the spot market showed typical volatility, long-term contract prices remained stable around US$80 for the first six months of the year, underscoring producer discipline.

Utilities have so far stayed largely on the sidelines, but expectations are mounting for a wave of contracting in the second half.

H1 2025 uranium pirce performance. Chart via Cameco.

H1 2025 uranium pirce performance. Chart via Cameco.

Uncertainty impacting utility sentiment

Trade tensions and tariff threats from US President Donald Trump have been a catalyst for volatility in the uranium market through the first half of 2025.

Term uranium contracting remains well below replacement levels despite firm prices and growing demand, according to Oceanwall’s Ben Finegold.

“Term prices are sitting around US$80 per pound right now—roughly US$6 to US$7 above spot—but it’s still extremely difficult to get reliable data on actual volumes and pricing,” said Finegold during the Bloor Street Capital Virtual Uranium Conference in June.

By mid-year only 25 million pounds had been contracted, putting the market on track to fall 75 percent short of replacement-rate contracting. That shortfall has been a recurring issue, with contracting volumes lagging for more than a decade.

While 2023 saw the strongest term contracting in years (160 million pounds), about 30 percent of that came from a single deal. In 2024, 110 million pounds were contracted, well above where 2025’s totals are likely to fall.

Uncertainty continues to weigh heavily on term uranium contracting, particularly among U.S. utilities, who remain unsure about the future of US-Russia relations and whether Russian supply will remain accessible.

“There’s a certain naivety among fuel buyers,” said Finegold, referencing a recent conversation with a former buyer who suggested utilities have grown used to a decade-long environment where they could easily dip in and out of the spot or term market.

But that era may be ending.

“I just don’t see a situation where the supply-demand fundamentals get better for utilities,” the source added.

Despite global momentum—31 countries aim to triple or quadruple nuclear capacity by 2050 and the US government has pledged US$75 billion toward domestic reactor builds—contracting volumes remain surprisingly low.

“It’s a pressure cooker,” said Finegold. “At some point something has to give—and when utilities return to the term market, history shows they tend to do so all at once.”

Supply gap to collide with surging demand

From a…

Read More: Uranium Price Update: Q2 2025 in Review