Lead Price Forecast: Top Trends for Lead in 2026

Lead prices were volatile in 2025 amid investor uncertainty and factors like tariff threats.

The base metal is primarily consumed by lead-acid batteries, but is also used to produce radiation shielding, weights and, in the defense sector, ammunition. More recently, it has seen increased demand from the electric vehicle (EV) sector as a low-voltage auxiliary power source for lighting, windows and other essential systems.

Because lead isn’t usually mined as a primary metal, its supply is tied to other metals like zinc, silver and copper, making lead prices highly dependent on demand for these other metals — and by extension, fairly volatile.

How did lead perform in 2025?

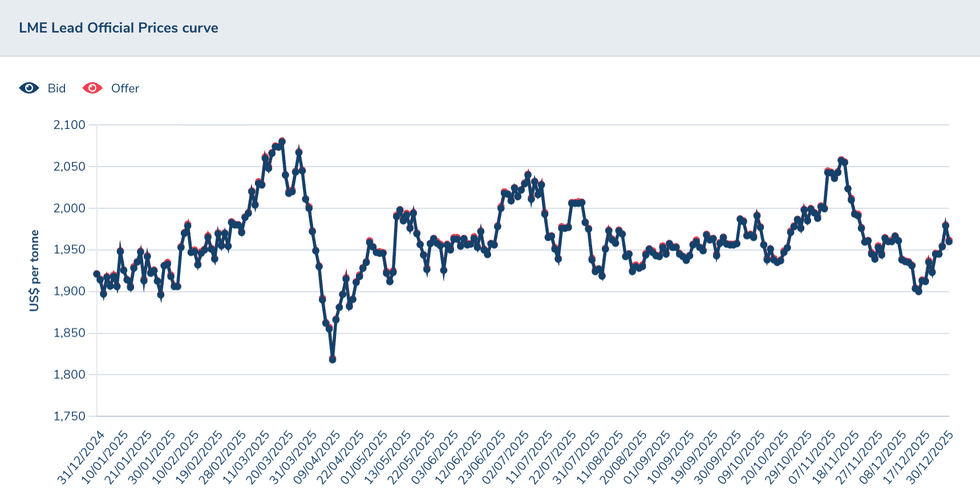

Continuous contracts for lead on the London Metal Exchange (LME) started 2025 at US$1,921.44 per metric ton (MT) and saw steady upward momentum, reaching a Q1 high of US$2,090.48 on March 18.

According to Shanghai Metal Market, lead’s early 2025 rise was supported by the end of the Chinese New Year holiday, as well as increased activity in the supply chain, which led to a limited increase in demand for lead ingot purchases. This actvitiy coincided with destocking of lead inventories in western markets, which further fueled the price.

Lead continued to trade above US$2,000 for the remainder of March, but the start of April saw its price floor fall out — the metal hit its 2025 low of US$1,829.75 on April 9 amid a broader rout in commodities markets. This came after US President Donald Trump’s “Liberation Day” tariff announcement on April 2.

LME lead price, 2025.

Chart via the LME.

Shanghai Metal Market notes that the tariff announcement came during the traditional off season for lead, with battery producers reducing production and weakening overall demand for for the metal. However, by the end of April, the lead price had rebounded as rising demand drove down inventories in downstream industries.

By the end of Q2, the price of lead had rebounded and was once again trading above US$1,900.

Trade concerns remained present, and although lead ultimately wasn’t included in reciprocal tariffs, there was still considerable uncertainty, dampening sentiment during lead’s normally peak August-to-September period.

During the year’s third quarter, a significant 45,150 MT delivery to LME warehouses in November pushed total volume to 266,125 MT, leading to a collapse in the lead price amid oversupply concerns.

The metal stabilized in the US$1,930 to US$2,050 range as the year drew to a close, spiking to US$2,078.84 on November 12 and to US$1,910.48 on December 12.

What trends will move the lead market in 2026?

According to the International Lead and Zinc Study Group (ILZSG), global demand for refined lead is expected to increase by 0.9 percent to 13.37 million MT in 2026 after rising 1.8 percent in 2025.

In an October report, the organization projects a 6.6 percent rise in US lead demand for 2025, driven…