Zinc Price Update: H1 2025 in Review

Zinc prices were in decline for much of the first half of 2025 as primary supply increased and demand from the construction sector slumped.

Primarily used to make galvanized steel destined for construction and manufacturing sectors, zinc has come under fire in recent years as inflation and interest rates took their toll.

The metal performed relatively well in 2024 as weak supply was offset by soft demand. However, as 2024 began, new threats to its performance emerged as the US began to look to tariffs to correct perceived trade imbalances.

Market performance by the numbers

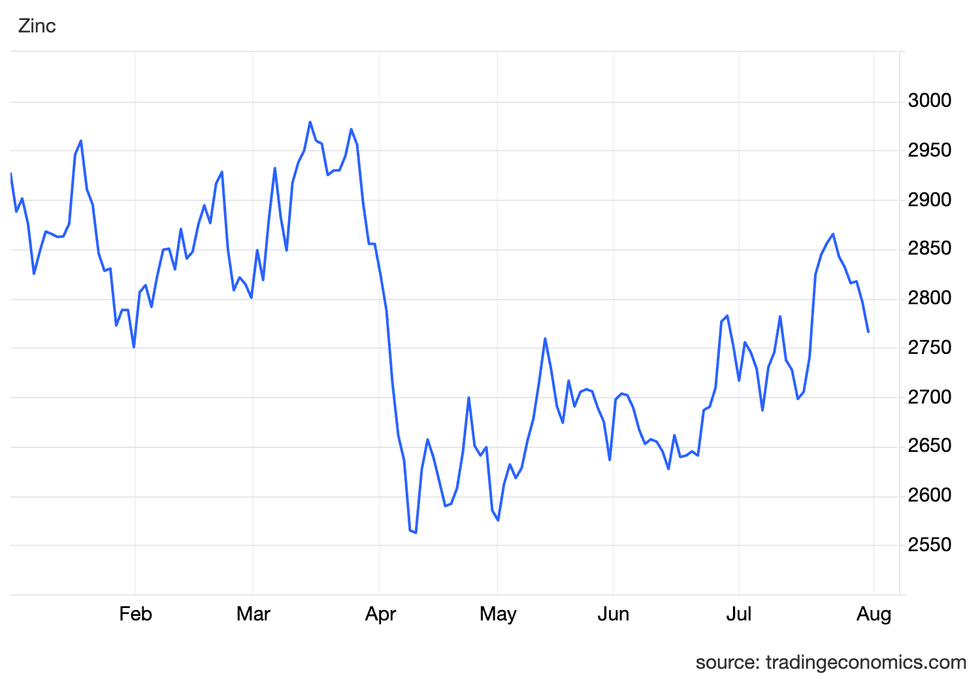

The zinc price started the year with downward momentum, sliding from US$3,150 per metric ton on December 10 to US$2,750 on January 31.

Zinc price chart, January 1 to July 31, 2025

via TradingEconomics

The metal found some support in February and March, climbing to US$2,928 on February 24 and then reaching a year-to-date high of US$2,971 on March 14; however, it wasn’t to last. The bottom fell out from under Zinc and quickly plunged to its year-to-date low of US$2,562 on April 9.

Since then, the zinc market has been volatile, and although it has recovered somewhat, it is still far from its first-quarter highs, peaking at US$2,865 on July 23.

What’s behind the price?

According to a review from the Shanghai Metal Market (SMM) on June 29, ex-China zinc concentrate production increased by 6.47 percent in the first quarter to 1.3 million metric tons versus 1.22 million metric tons during the same period of 2024.

It attributed these increases to resumption in production at Boliden’s Tara mine in Ireland, and ramp-ups at Grupo Mexico’s Buenavista mine in Mexico and Ivanhoe’s Kipushi mine in the Democratic Republic of the Congo.

Additionally, SMM noted that Xinjiang’s Huoshaoyun lead-zinc mine started production in May, with output reaching 50,000 metric tons in its first two months and is expected to reach 150,000 metric tons in July. The company is targeting full-year production of 700,000 to 750,000 metric tons.

Although supply seems robust and Chinese imports of concentrates increased 52.46 percent over 2024, treatment charges for imported metal have also increased from US$20 per metric ton at the start of the year to US$65 in May. The sharp increase in fees indicates an oversupply in the market, allowing smelters to charge more.

The SMM findings are further supported by data released from the International Lead and Zinc Study Group (ILZSG), which reported on June 18 that mining supply had increased during the first four months of the year to 3.94 million metric tons from 3.75 million metric tons in 2024.

It also showed flat demand for the metal with 4.28 million metric tons consumed during that period versus 4.3 million metric tons last year.

Changing US policy

A steep decline in…

Read More: Zinc Price Update: H1 2025 in Review